Investing 101: Risk and the Possibility of Loss

Contents

In the financial planning world, the concept of risk is often used in conversation. Risk has multiple meanings, but the first definition in the Merriam-Webster dictionary is quite simply the “possibility of loss.”

In this article we are going to explore both the “possibility” and the “loss” noted above.

Before we recommend investments or determine the allocation mix between stock, bonds, and cash, we often turn to psychology in our discussions.

We seek to learn from investors':

- Experiences in the past.

- Expectations for the future.

- Levels of understanding.

- Degrees to more subjective or objective in decision making.

Then finally, the last and easiest one, when and how much money will they need to spend? It is the easiest because that problem is simply a calculation with a clear quantifiable answer.

Once we’ve gone through the exercise, the decision is made, and the journey begins.

As a portfolio manager, there is a possibility of loss in every investment. Every investment, including cash, has some possibility that your money will not be returned. For cash, it could be stolen, misplaced, or even caught on fire. For a money market fund, withdrawals could be gated, which means that the fund stops redeeming the funds, or the fund goes out of business.

As an example, I keep a collection of antique currency on my office wall. Many in my collection are worthless from broken governments, countries that switched currency, or were inflated out of existence such as my 10 billion dollar note from Zimbabwe. All kept as a reminder that there are risks in everything.

Since there is risk in everything, it’s the possibility of those risks that make the difference. The chance of your US dollar bill losing its value, the loss, versus your shares of AMC Theatre are wildly different. As portfolio managers, our primary job is to understand not only the probabilities of these events, but also the degrees of loss that could happen, and then make sure they are balanced and acceptable enough for investors.

This understanding comes from a constant level of learning to stay up on current economic events, new investment products, research papers on new theories and practices, and the one that our clients see the most of, which are the “How are you doing?” conversations. These conversations are there to better understand investor expectations, understanding of what’s going on, and how to help them make the best decisions.

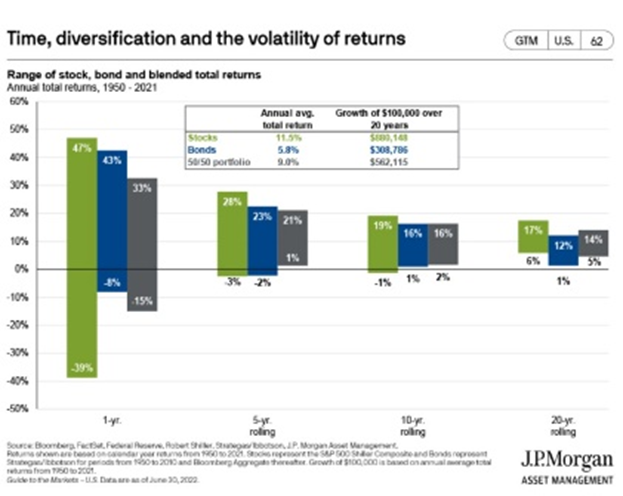

Let’s look at the second aspect of the definition which uses the word “loss.” Many see that word to mean “giving money to buy something, and not getting anything back in return.” In the short term, there is a heightened possibility of this when investing, but over long enough timelines, this risk is minimal as shown in the chart below from J.P. Morgan. The chart shows that since 1950 there has never been a rolling 20-year period where people had a negative return at the end of 20 years, and only one period with a negative 10-year rolling return which was the period between the DotCom and the Great Recession.

Looking at the type of investments we make, in the short term some go down, some go up, some go sideways. In the long run, however, since they are so diversified the risk of loss is very minimal. As an example, if you own the S&P 500 index fund, to lose all your money, 500 of the largest publicly traded companies in the United States would all have to go bankrupt. The odds are so low that the figure is meaningless.

We can all probably agree that the chances of your S&P Index fund completely going away is very low, and that over time their values have had positive returns. This all brings us back to the only real risk of “loss” which is having to sell when the market is down to have cash to spend.

This decision is where the most risk is taken. The decision of what your investment mix or allocation is between stocks, bonds, and cash not only in the beginning but also if any changes need to be made as your life changes.

Oddly enough, as portfolio managers and financial planners, this is a simple set of calculations that can be done, and a precise figure can be generated. This is all done based on the size of your portfolio and when you need cash from it. Often this figure is calculated regardless of your age, besides the fact that the younger you are, the more cash may be needed for a longer time period.

For instance, if your pension and social security cover all your costs, and you have adequate insurances, then regardless of if you are 65 or 95, and you have some “emergency money,” it is okay to have more stocks than bonds. If you have a higher level of cash needs each month, then you will need more bonds than stocks and we can tell you the allocation mix you need to the exact dollar amount.

The overall mix of your portfolio between stocks, bonds, and cash is often the most important decision. In 2015, Vanguard demonstrated that this mix accounts for 91% of your return over the previous 25 years. The risk of this decision is if you have too many stocks you may have to sell them when they are down. If you take too little risk and have too little stocks, then you may not earn enough to generate sufficient growth.

Regardless of what the calculations show, there is a subjective side to all of this. As mentioned at the beginning of the article, depending on your experiences, expectations, levels of understanding, and subjective decision making you will have a different allocation mix. Often if a client wants to “err on the side of being more conservative” then if the conditions can be met, there is no harm in that. On the flip side, however, we will not allow an investor to take more risk than they need.

There are many factors, both objective and subjective, that go into the determination of the levels of risk you should take. As portfolio managers, we take into consideration all of them, and work with you to determine the level that is right for you.

If you want more information on how we go about this process, please feel free to call and talk with one of our team members.

About the Author