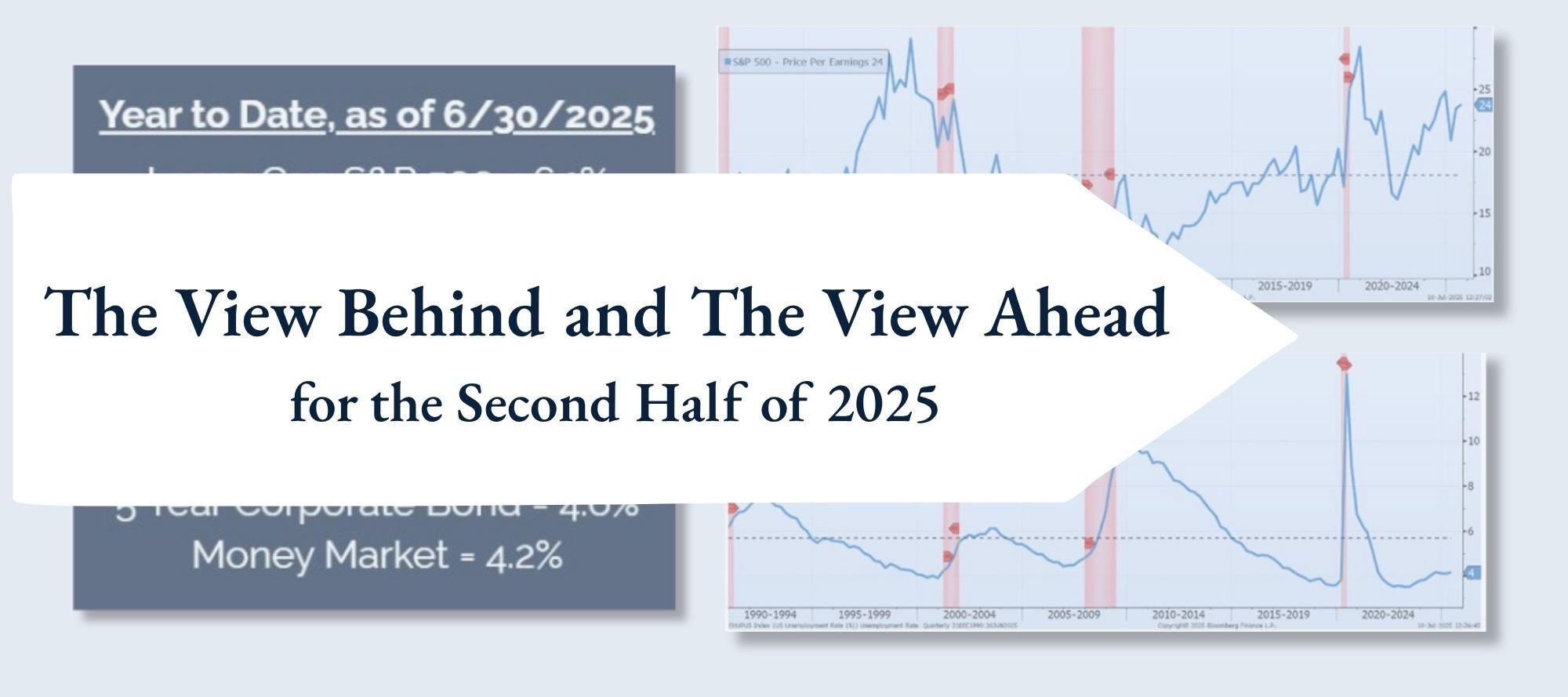

Chart of the Day Extra: The Year-to-Date Recap

Contents

As we closed out the first half of 2025, all I could think is, “That was a wild ride!”

2025 First Half

After strong gains in January and February from the market’s hope of less regulation, the market peaked at 4.5%. Then, in a series of historic drops, it bottomed out down 20%. Shortly after, it rocketed back up to a record high for a year-to-date return of 6.1% at the end of June. We experience “bear” markets every few years, the last being in 2022 with a 24% downturn, but they usually play out over a longer time span.

The one in 2022 took 10 months for us to reach the bottom and 14 months to fully recover. This last one, earlier this year in 2025, took two months to go down and only two months to fully recover. In fact, after all the 15% declines in the past, this was the fastest recovery ever in the history of the stock market. It usually takes anywhere from six months to a year to see new highs.

What Caused This?

It all began with the stroke of a pen that created tariffs, which led to some dark days in the market, and, oddly enough, it was resolved just as quickly by a second stroke of a pen that eliminated them.

Just like the COVID downturn, these two were not caused by “structural cracks in the economy,” they were man-made. Structural cracks take more time to realize, adjust, and recover from. Examples would be the Great Recession, where the foundations of the banking system broke, and the last downturn in 2022, where the world had to adjust to the realities of higher interest rates not seen in over 15 years.

How Did We End Up?

During the downturn, many client discussions turned to how well the bond reserves held up and how bonds were available for sale to generate any needed cash. Our use of ultra-low-cost, well-diversified, investment-grade, liquid bond exchange traded funds (ETFs) performed exactly as planned, saving clients who held them from having to “sell low.”

2025 Second Half

Three things to think about as we look ahead to the second half of 2025:

- The Floor. A market floor is being realized. A unique aspect of the recent downturn was that a majority of institutional and hedge fund managers sold, while retail investors continued to buy. Many of those who sold now have red faces, but the final chapters of the 2025 story have yet to be written, and they may still be proven correct. However, as time passes and the market continues to reach new highs, the likelihood that they were correct to sell diminishes. Helping to support this floor is a still record amount of money ($7 trillion) sitting in money market funds, much of it waiting for buying opportunities if the market goes down.

- The stock market continues to be “expensive” based on the historic metrics. Does this mean not to invest in stocks? No, it means not to speculate and overweight stocks at the expense of your bond reserves.

- All eyes are on unemployment. The famous saying is “you can’t have a recession if everyone has a job,” which is why this metric is so closely followed.

Our Goal

Our goal continues to be to navigate risks and opportunities while ensuring your portfolio includes the most efficient, cost-effective, transparent, liquid, and high-quality funds available. We allocate these specifically to your needs and situation to reduce risk and maximize returns.

I’m looking forward to another interesting six months before 2025 comes to an end. We believe the most successful investors are those who understand what they are investing in and why. Don’t hesitate to call your portfolio manager if you have questions.

About the Author