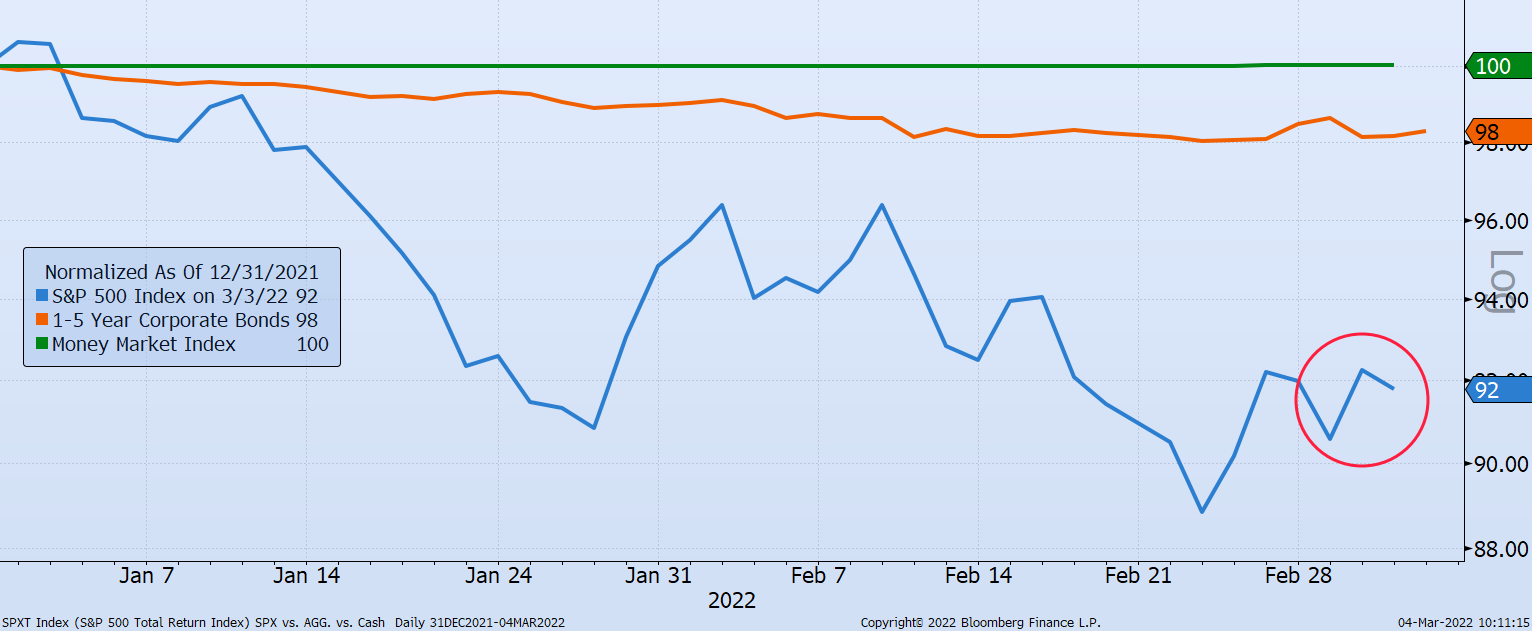

The Market Response after Eight Days of Conflict

It’s hard to do commentary when in the morning, the markets are down, and by lunch they are level, and by the close they might be up, and vice versa.

Today's Market Notes - Russian Edition

As with all things, patience is the name of the game in the long run. Below are three notes about today.

October Investment Update

After declining in September, the equity market is now celebrating the economic recovery from the COVID virus and solid growth in U.S. corporate..

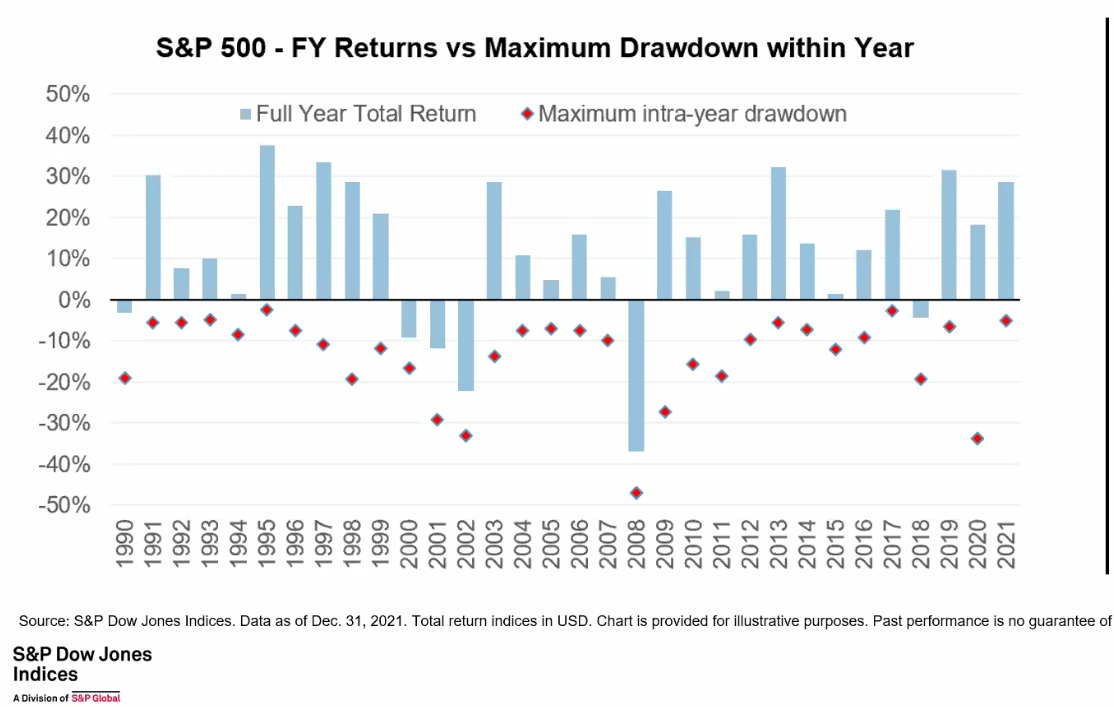

2021 Year-End Market Review

The equity markets ended the year with strong performance despite the uncertainty about the new variant of COVID and the Federal Reserve’s..

November 2021 Market Update

The better-than-expected third-quarter corporate earnings reports were evidence of a broad-based economic recovery causing investor psychology to..

October 2021 Investment Update

After declining in September, the equity market is now celebrating the economic recovery from the COVID virus and solid growth in U.S. corporate..

Third Quarter Ups and Downs

The S&P 500 Index is consolidating as Washington policymakers postpone important decisions on the budget ceiling and the infrastructure bills. The..

Market Update for Third Quarter 2021

The S&P 500 Index is consolidating as Washington policymakers postpone important decisions on the budget ceiling and the infrastructure bills. The..

Market Update for Third Quarter 2021

The S&P 500 Index is consolidating as Washington policymakers postpone important decisions on the budget ceiling and the infrastructure bills. The..

Pent-up Demand Fuels Economy

Economic indicators are proving that consumers and businesses are fueling the economy with pent-up demand on spending. Consumers are reacting to the..

The best-performing sectors were energy, financial, healthcare, and materials.

The S&P 500 Index gained 8.1% for the second quarter and 14.4% year-to-date despite concerns over Federal Reserve policy, fiscal spending and the..

First quarter corporate earnings exceed expectations

The S&P 500 index was up slightly in the month of May due to growing investor confidence in higher 2021 corporate revenues and earnings. With the..

Fed Remains Resolute in Bond Purchases and Yields

Most first-quarter corporate earnings reports have been meeting or beating expectations and this has raised the confidence that equity valuations are..

Federal Spending Strengthens U.S. Dollar

The S&P 500 Index grew 5.8% in the first quarter in response to the massive fiscal stimulus and the anticipation of a significant economic rebound...