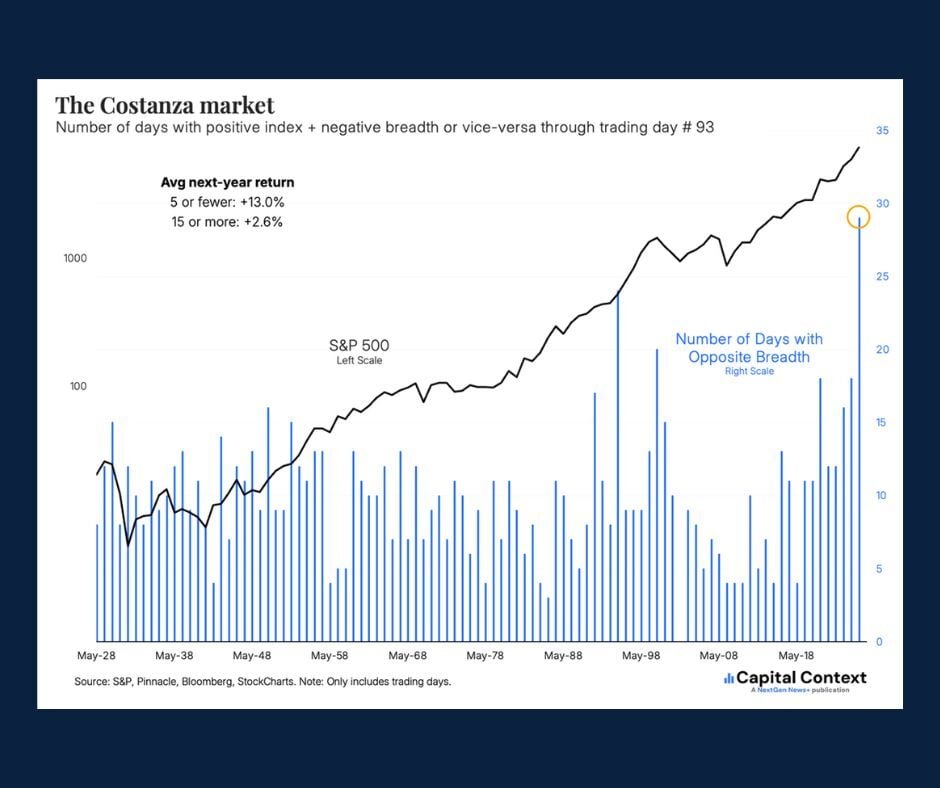

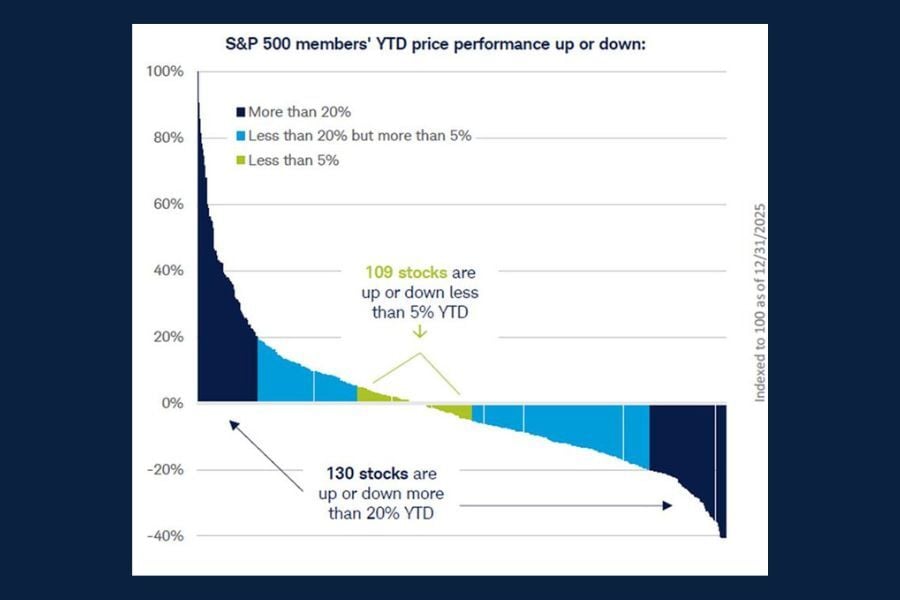

Chart of the Day: The Costanza Market

Today's Chart of the Day is from Jason Goepfert on X: "It has been a Costanza market* to a historic degree. Never before has the S&P 500 index gone one way while its stocks went the other on so many days this far into a year."