Chart of the Day: S&P By Decade

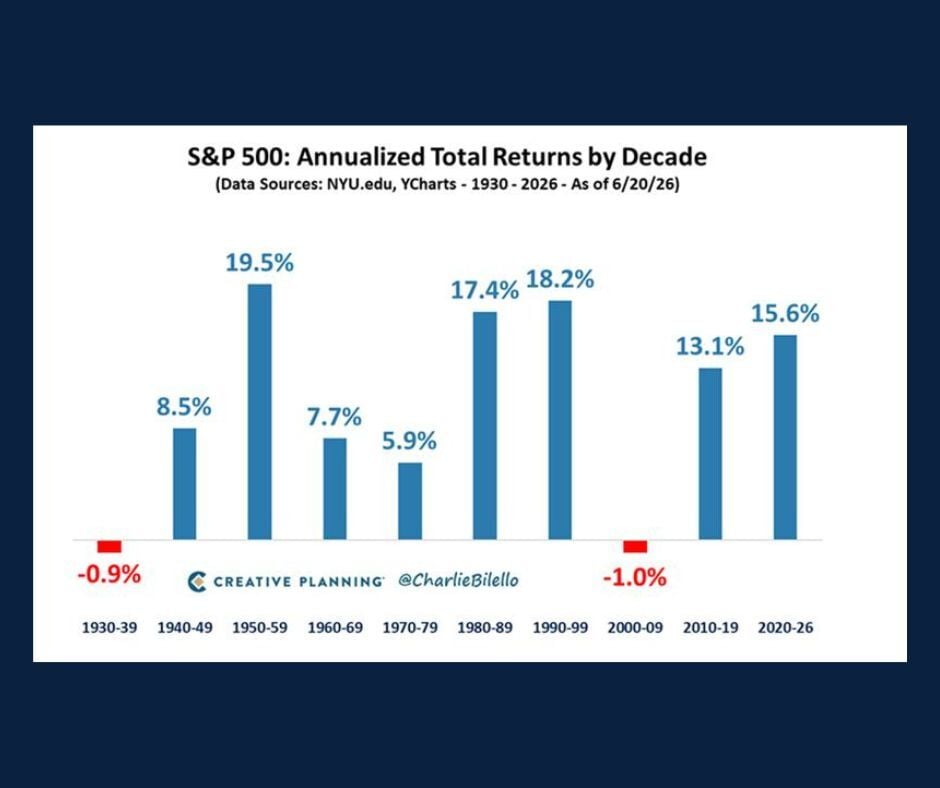

Today's Chart of the Day from Charlie Bilello’s blog, "The Week in Charts," from June 24, 2026, examines the S&P 500's performance by decade, with returns dating back to the 1930s.

Today's Chart of the Day from Charlie Bilello’s blog, "The Week in Charts," from June 24, 2026, examines the S&P 500's performance by decade, with..

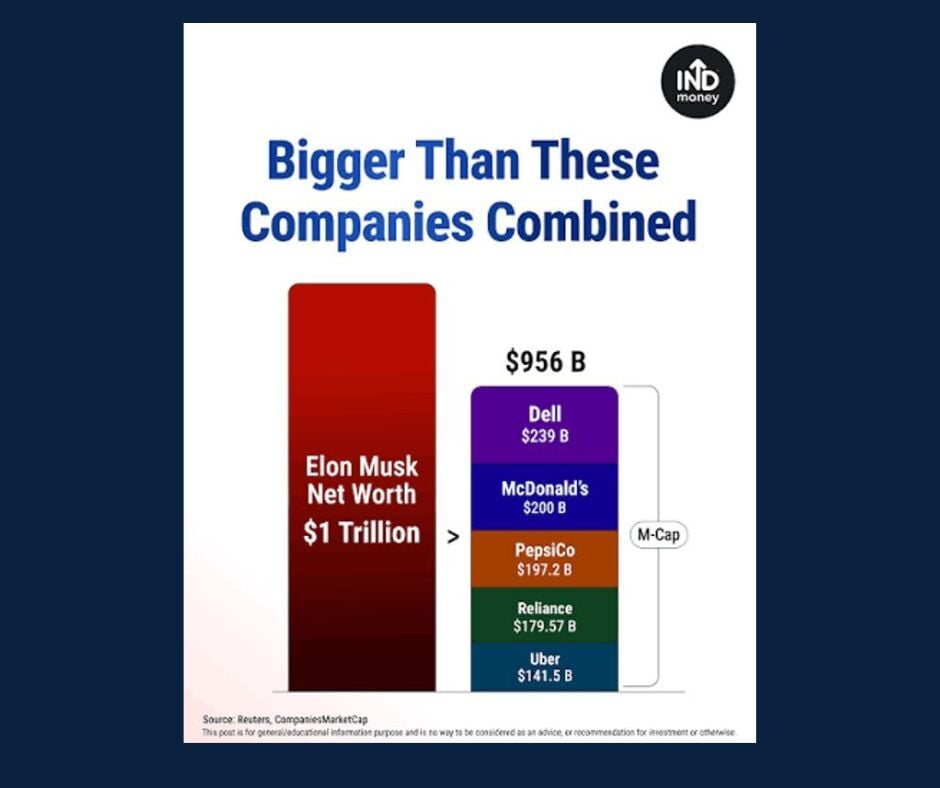

Today’s Chart of the Day comes from indmoneyapp on Instagram and compares Elon Musk’s ~ $1 trillion net worth to the market values of five well known..

Today’s Chart of the Day from the Tax Foundation’s "2026 Sales Tax Rates | Sales Taxes by State" highlights combined state and local sales tax rates..

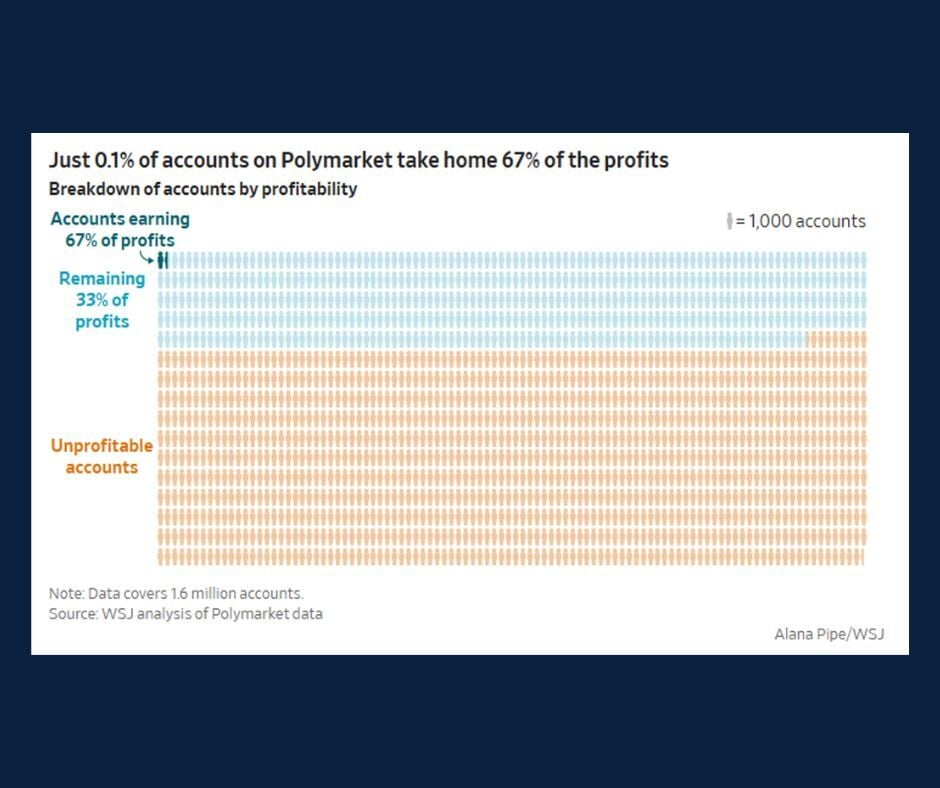

Today's Chart of the Day from The Wall Street Journal article "Why Almost Everyone Loses—Except a Few Sharks—on Prediction Markets" explores what..

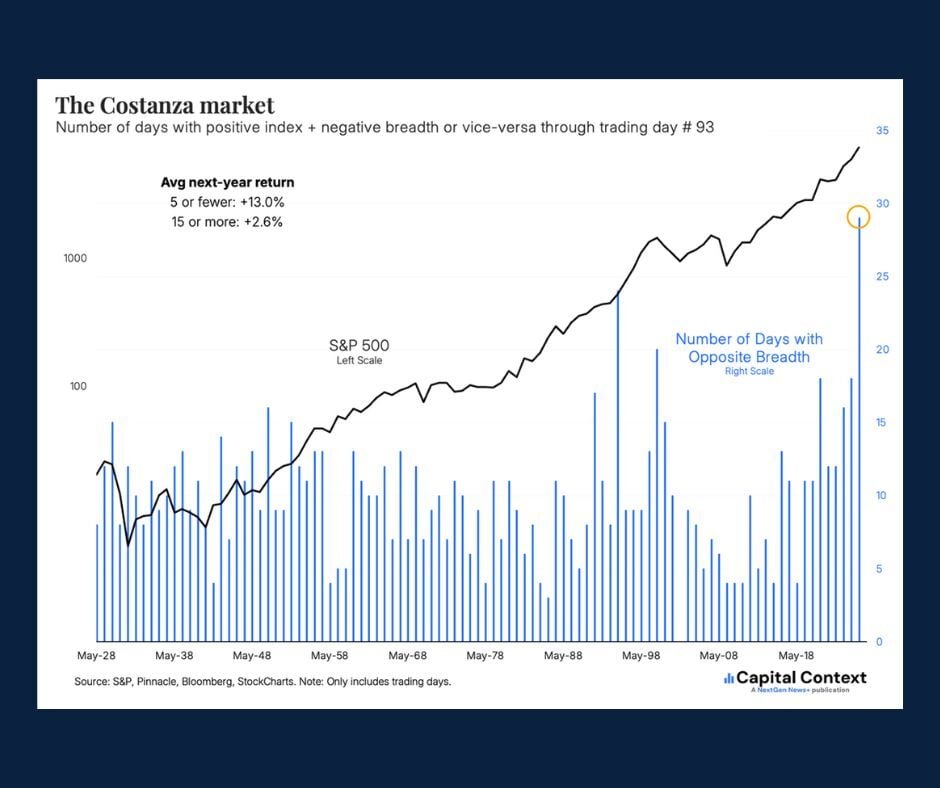

Today's Chart of the Day is from Jason Goepfert on X: "It has been a Costanza market* to a historic degree. Never before has the S&P 500 index gone..

Picture this: It’s a busy Saturday morning at your weekend market booth. A customer falls in love with your handmade products, picks out three items,..

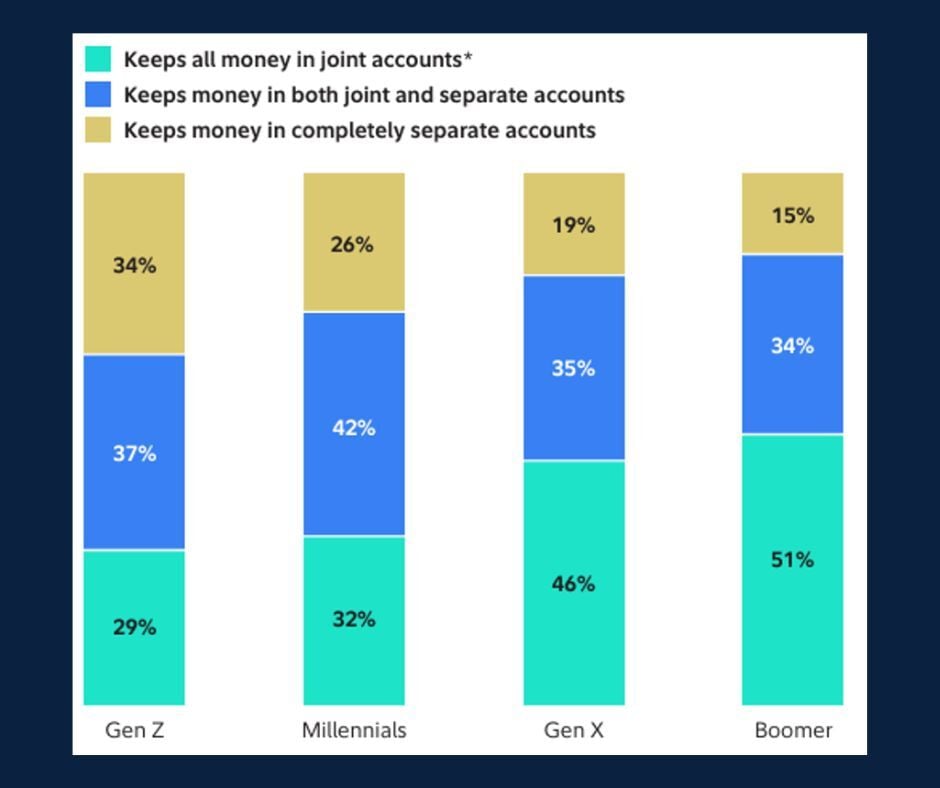

Today's Chart of the Day from Fidelity’s "2026 Couples and Money Study" highlights some key findings on how couples manage their money.

Today's Chart of the Day, "Metro-Level Summary: 50* Most Populous Metros (March 2026)", comes from The Week in Charts (6/8/26) - Charlie Bilello's..

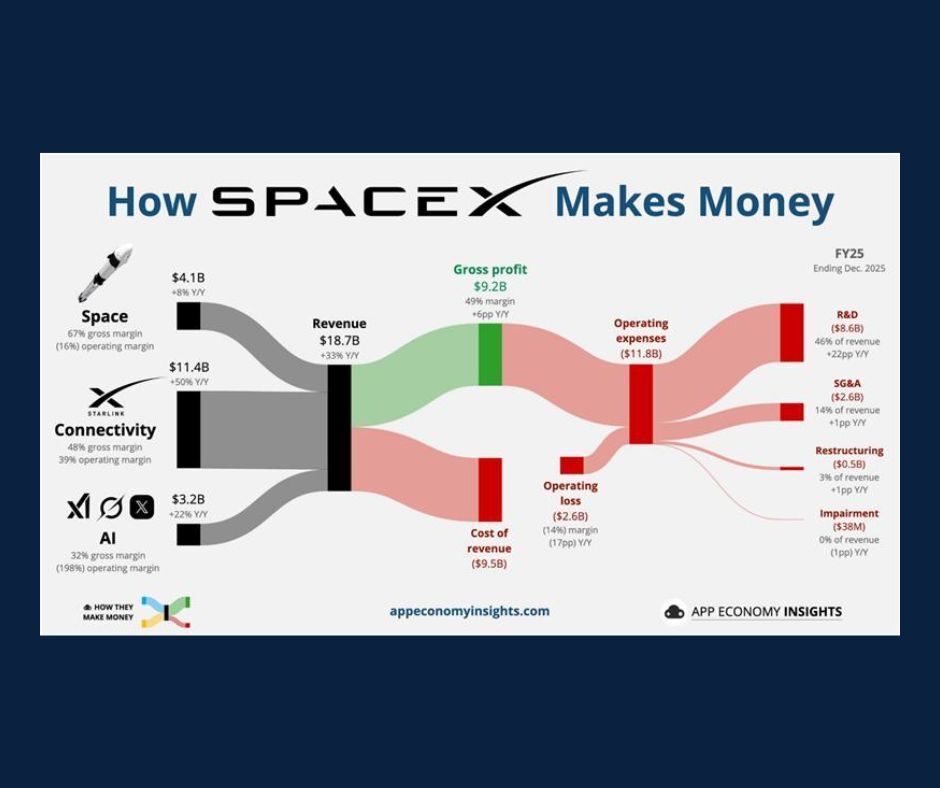

Today’s Chart of the Day is "How SpaceX Makes Money" from an article in App Economy Insights and illustrates the key drivers behind the SpaceX..

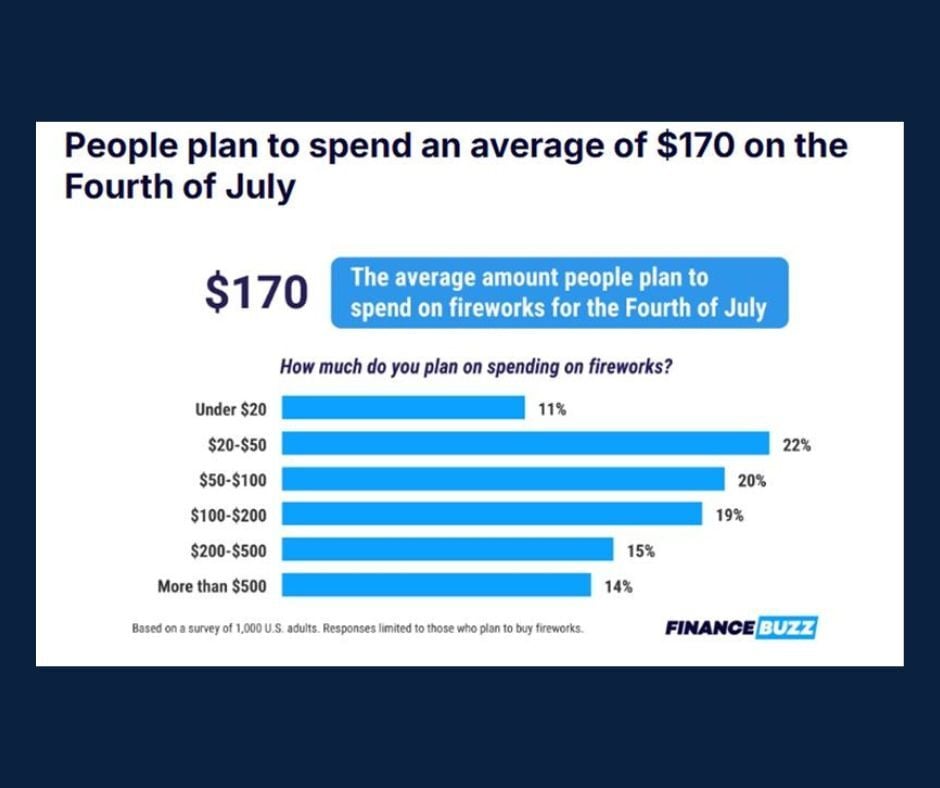

With the 4th of July approaching, and as we prepare to celebrate America’s 250th anniversary, today's Chart of the Day from a FinanceBuzz blog,..

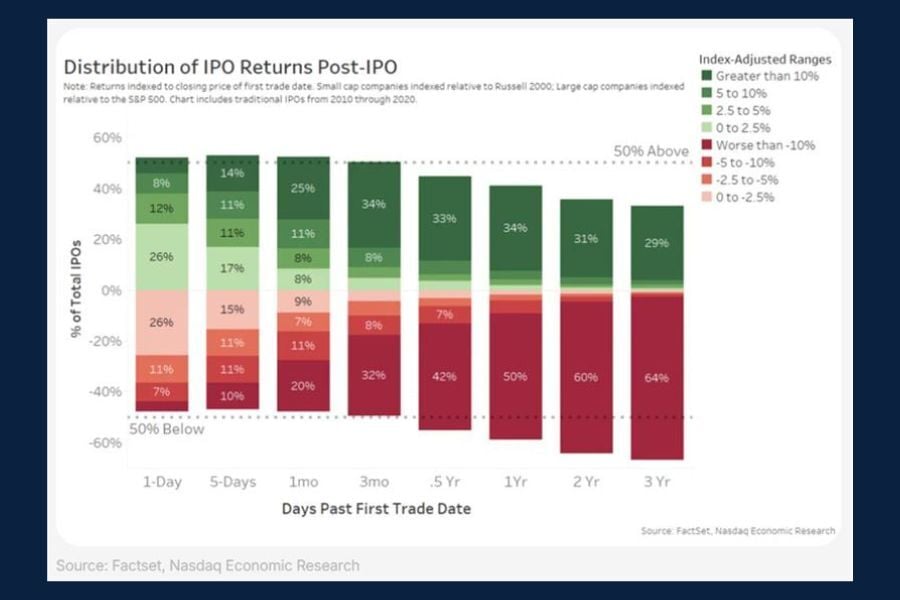

Today’s Chart of the Day, found in arvy weekly's "The IPO Class of 2026" illustrates how stocks have historically performed following an IPO, or..

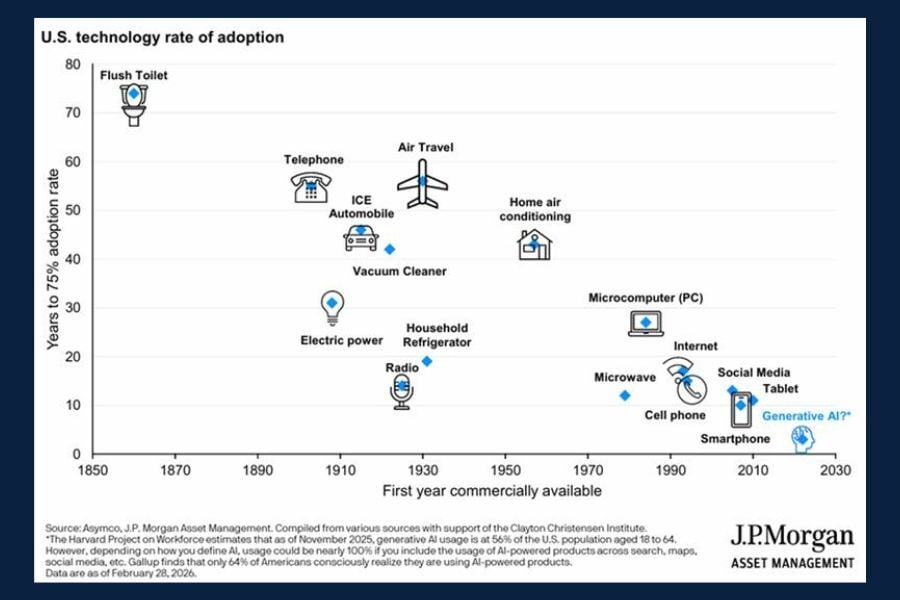

Today’s Chart of the Day from J.P. Morgan Asset Management highlights decades of technological innovations that have shaped modern life.

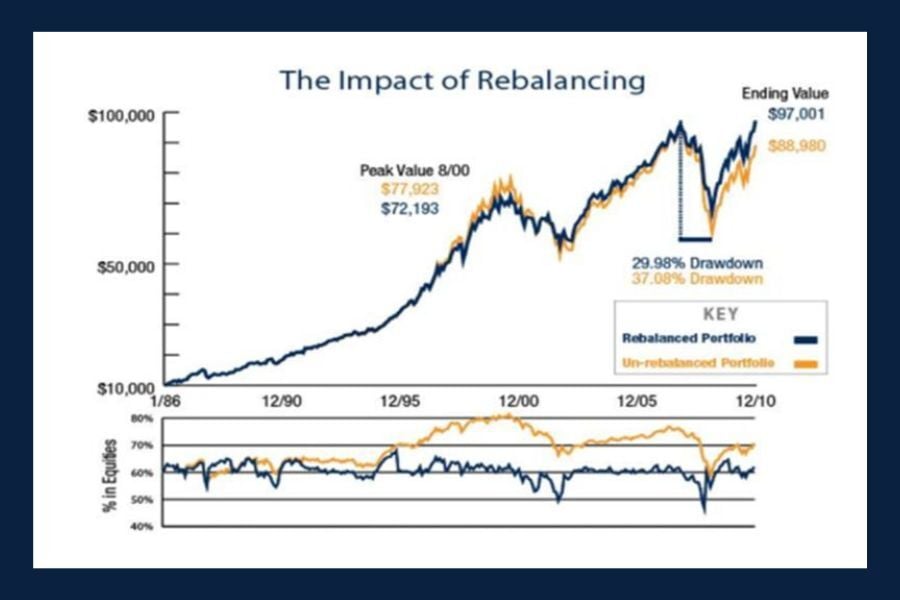

Today’s chart from AllGen Financial’s "Maximizing Investments with a Rebalancing Strategy" illustrates a 25‑year simulation of a 60/40 portfolio to..

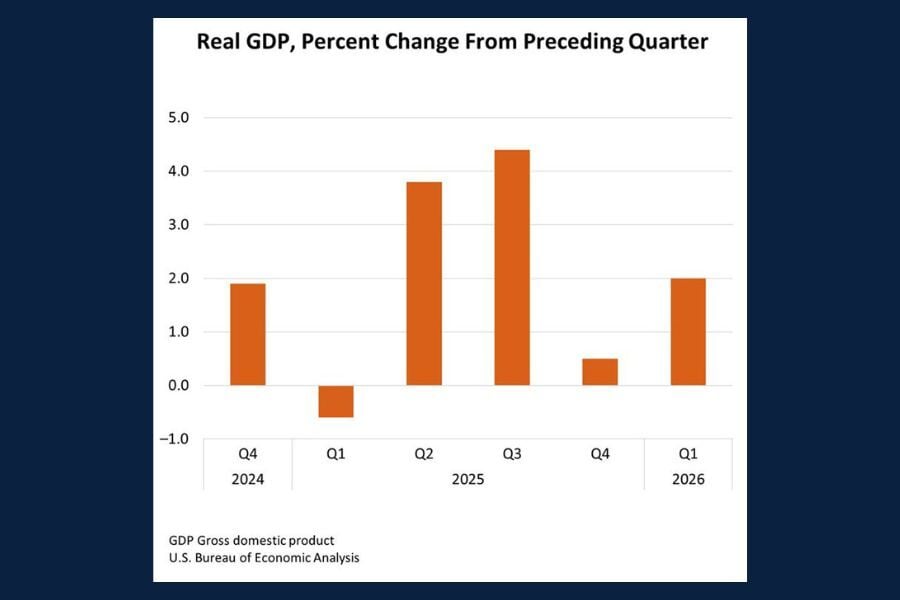

Today’s Chart of the Day comes from the Bureau of Economic Analysis (BEA) and shows the published results for real Gross Domestic Product (GDP) in..

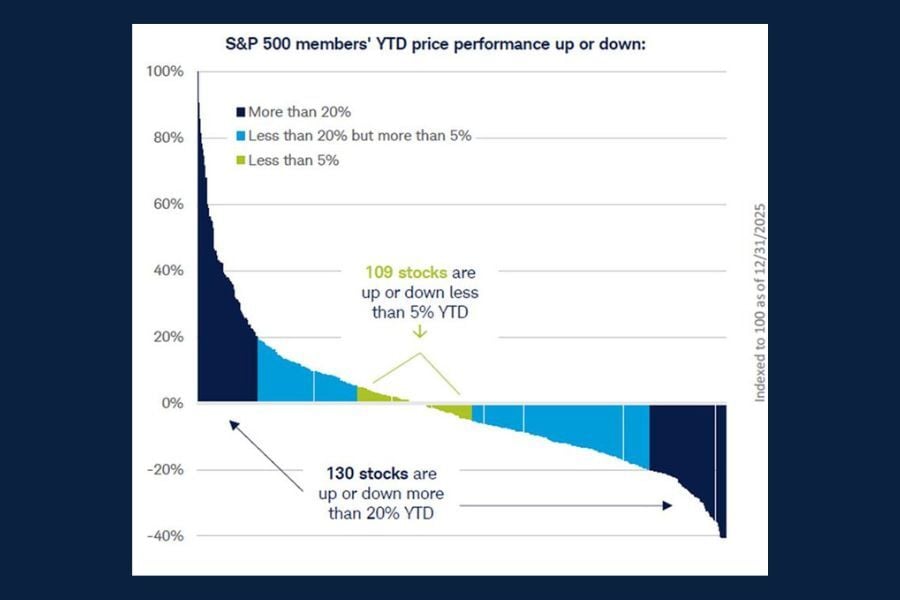

Today’s Chart of the Day from Schwab Market Insights illustrates individual stock performance across all 500 constituents of the S&P 500 index during..